A few years ago, I wrote a blog post about how I received a shattered insulin vial in my mail order pharmacy delivery. At that point in time when it initially happened, I’d never experienced anything like that before and was immediately panic-stricken about how I could get a replacement for something that wasn’t my fault, as the vial was smashed upon arrival.

Fortunately, a quick phone call resolved the situation, and I’ve been lucky enough to receive fully intact insulin vials in the mail every 90 days or so ever since. But imagine my fear and concern when I got my most recent insulin delivery and discovered, upon opening the package, that one of my insulin vial’s cartons was totally squished!

The smooshed packaging, in question.

I have no idea how it happened to just one out of the five in the order, seeing as they were all put into the package with the exact same level of cushion and protection. The 5 vials were in a zip-top plastic bag, which lay on top of 3 ice packs, which were surrounded by layers of soft foam packing material, all of which was placed in a mid-size cardboard box. It’s not like the squished insulin carton was separate from the other four in any fashion, so truly, I’m at a loss as to how it got so severely misshapen. But what I can say is that I was beyond relieved when, after further inspection, I found that the vial was fully intact – not a drop of insulin missing from it nor a crack in the glass to be found. Phew! Momentary worry faded into reassurance that I wouldn’t have to make any phone calls to obtain a replacement, and that all I had left to do was put my new insulin vials in the butter compartment of my fridge (naturally) with my remaining old vials.

Squished upon arrival, but definitely not destroyed – though a good reminder nevertheless to always inspect my insulin when it’s delivered, just in case any surprises await me.

Hi, my name is Molly and I have type 1 diabetes, and although I am extremely grateful for health insurance, I also hate every aspect of it.

When I aged out of my parents’ health insurance plan two years ago, I was completely lost and overwhelmed by choosing my new plan. How much would I have to pay for my supplies? Would everything be covered? Could I keep my doctors? How much money should I put into my FSA? The answers to these questions took me a good chunk of time to figure out, and I only started feeling good about my knowledge of my old job’s health insurance plan in the last year or so.

As a result, the only thing that made me less excited to start my new job was the burden of having to figure out a new health insurance plan. And for good reason, it turns out, because it has been a challenge to say the least. But there are a handful of things I’ve learned along the way that I don’t think I’ll ever forget so that I can have an better experience the next time I need to change health plans. Here are my tips for making the transition from one health insurance plan to another as easy as possible:

1.Take stock of ALL my supplies before starting the new job (and before losing my old job’s health coverage). This was, without a doubt, the best thing I could’ve done for myself before I started my new job. In my last few weeks with my former company, I looked through all of my diabetes supplies and inventoried them. I kept a running list of the most important items (things like insulin, Dexcom sensors/transmitters, and pods) and decided that even if I had plenty of those things, I would still place an order for them before losing my health insurance. This ended up being a fantastic idea because it took me a solid couple of weeks at my new job to figure out which health plan would work best for me, and in that span of time, my supply stash was dwindling. On top of that, it took several more weeks for me to get all my prescriptions straightened away (more on that in tip 3), so I was especially grateful that I had seriously stocked up before leaving my old job.

2.Compare plans extensively. Like I mentioned above, I spent a couple weeks reading through my plan options before I finally settled on one. It took me so long because I wanted to feel 100% comfortable with my new plan, and I knew that I had a 4-week period to complete my research before committing to a new plan. Plus, my new job uses a website that offers a health insurance plan comparison tool (a super cute one, to boot, that explains all things insurance in layman’s terms) that I was happy to take advantage of during the decision-making process.

What tips would you have for someone who is switching health insurance plans?

3. Send as many messages and make as many phone calls as it takes until everything about the new plan is crystal clear. For me, this including calling my local pharmacy and sending toooons of online messages to my doctor’s office, as well as my new health insurance provider. I honestly felt like I was playing a game of telephone – you know, that game that kids play where they have to whisper a message into each other’s ears as a test of listening and communicating effectively – because it seemed that nobody would take accountability for sending my prescriptions to the right place or understanding exactly how I needed help. So in the last few weeks of July (leading into the first few weeks of August, really, ‘cuz I’m still working on this), I made a vow to myself that I’d get to the bottom of everything and get my prescriptions fully straightened away. I’m happy to report I’ve made substantial progress, but I’d be lying if I said it didn’t require a lot of my spare time and energy.

4. Talk to coworkers and ask for their feedback on plans. This might be unique to me because I work for a diabetes organization and my colleagues have an intimate knowledge of health insurance hurdles combined with a chronic illness, but even so, I remember asking coworkers at my previous job about their thoughts on the health insurance offerings and I got some solid feedback from that. So that’s why I decided to ask around at the new job, and of course I was met with helpful replies that made my transition a little smoother.

The biggest lesson I learned throughout this process? I realized I need to give myself a little grace. This stuff isn’t intuitive to anyone (unless you’re some sort of health insurance guru). I shouldn’t beat myself up because the system is more complicated than it needs to be. And bottom line is that I need to focus on the fact that I have choice when it comes to health insurance, period, because I know that there are too many people out there who can’t say the same.

So I guess in a way I am glad for the challenges presented to me by my health coverage.

Have you ever received an email that made you stop breathing for a moment? Did it feel like time stood still as you blinked rapidly and tried to comprehend the meaning behind it?

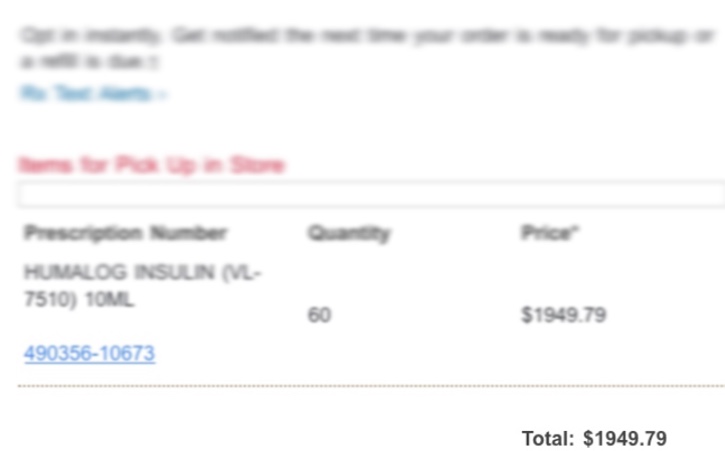

It sounds like a dramatic overreaction, but imagine getting a notification from your pharmacy notifying you that your prescription would cost almost $2,000. That’s a big old chunk of change. The mere thought of paying that much for a supply of insulin makes my heart race and my palms sweat.

I nearly keeled over when I saw this dollar amount.

I’m happy to report that this was a giant mistake; for whatever reason, my doctor’s office sent my prescription for Humalog to my local pharmacy, even though I explicitly told them that I use Express Scripts for my insulin orders. It was a total mix-up, and the approximately $2,000 was an amount that I would pay if I didn’t have any insurance coverage. I do, and though I’m not sure how much I’ll be paying for my insulin yet, I know that it can’t possibly cost this much.

I’m relieved that I was able to call the pharmacy and straighten this out without spending a cent of my money. But it was also a major wake-up call to a reality that many people are forced to face when it comes to refilling insulin prescriptions. It’s not fair. (That last sentence is the understatement of the century.) I can’t make any sense of it and I don’t know how many people have no choice but to fork over such a large sum of money on a monthly basis in order to live. Thoughts of those individuals and their dire situations scare me far more than navigating the world of health insurance ever could.

While I didn’t appreciate the mini heart attack this email triggered, I guess I am glad that it alerted me to the fact that I’m going to have to be aware of things like this going forward. As I figure out my health insurance costs and coverage, I anticipate more confusion, surprises, and expenses…but hopefully I can also expect/experience a pleasant discovery or two along the way.